According to U.S. Census Bureau estimates, the number of Americans age 65 and older will…

Long-Term Care Crisis in America

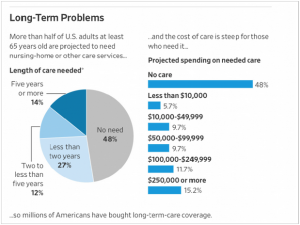

There is a crisis facing Americans requiring long-term care (LTC) coverage. Industry-driven, massively underpriced policies are playing fiscal catch up with hefty premium rate increases. This price increase is forcing some aging Americans to abandon their policy while others struggle to reduce their amount of LTC coverage to keep their rates affordable or reduce their future lifestyle by dipping into their retirement savings. Abandoning LTC policies turns out to be the last resort for many policyholders as they understand how valuable they are and that a policy lapse would cause them to lose all of their monies paid to the insurer.

Throughout the insurance industry, the metrics applied to the long-term care business model underestimated how long policyholders would live and the number of claims they would submit. Policyholders are living years longer than the actuaries had projected. Compounding the crisis of this flawed business model is years of very low-interest rates. On an inflation-adjusted basis, return on investment has fallen vastly short of needs for all long-term investors, including pension funds, life insurers, and the average American saving for retirement. The financial fallout is that fewer people are seeking long-term care insurance policies and those that are, typically pay more and receive less coverage.

Further compounding long-term care problems is the escalation of Alzheimer’s diagnoses and other dementia diseases, which invariably increases an individual’s need for long-term care. Medicare does not make provisions for coverage in long-term care facilities. Even if you position yourself financially to qualify for Medicaid, which does provide for LTC, there is often a long waiting list and reportedly not a high standard of care when you become a resident.

Senator Patrick Toomey (R-PA) is preparing legislation that includes a clause to allow people to pay for long-term care insurance via a tax-free withdrawal from their 401(k) retirement plan. The withdrawal, up to 2000 dollars a year, would not be subject to income tax, and the limit would be indexed for inflation over the years.

The Internal Revenue Service is also trying to offset tax liabilities for Americans that cover long-term care insurance premiums in 2020. There is a range of tax-deferred dollar amounts depending on your age, and this information is posted on the American Association for Long-Term Care Insurance website.

Relying on the federal government to fix the long-term care crisis is a cautionary tale. McKnight’s Senior Living reports that the LTC sector typically gets very little play in Washington, DC. Hospitals, doctors, insurance companies, and drug companies with big lobby monies are far more likely to receive legislative attention, often to the demise of long-term care operators and the vulnerable American population they support. Beyond the untenable high costs of LTC premiums, excessive administrative costs burden the US health care system. Washington DC, notorious for its complex, plodding policy progress, will not likely address the situation beyond creating tax-deferred access to retirement accounts and other tax incentives. Instead, the government is okay to allow the paying public to absorb the high costs of long-term care as the industry sector tries to salvage itself.

One of the worst outcomes of these scenarios is that long-term care has become such an expensive problem that Americans are shying away from proactive planning to address the very likely need they will require long-term care insurance in the future. The US Department of Health and Human Services has a website that addresses long-term care basics and provides resources, tools, and links to guide your LTC planning.

Other solutions can provide the essentials for long-term care packaged in different insurance programs. Short-term care insurance, or convalescent insurance, provides a long-term care type of coverage for 180 to 360 days. Because there is no long-term commitment to the insurance companies, premiums usually are less than traditional LTC. Critical-care or critical-illness insurance are two similar types of insurance coverage offering lump-sum cash payments to those who are diagnosed with a stroke, heart attack, and other serious illnesses. The benefits range can be six months up to two years, depending on the company and policy chosen. The drawback to these insurance policies is they do not cover pre-existing conditions. Deferred annuities for after retirement and annuities with long-term care riders can also be alternative solutions to traditional LTC insurance.

The time to get proactive and creative about long-term care insurance is now. Current statistics may give a false sense of security regarding the likelihood you will need long-term care. Projections are indicating between 65 to 75 percent of Americans will require some level of long-term care after retirement. The unspoken truth that many within the LTC industry and government do not address publically is that if the problem is not resolved, it will still ultimately go away because the person who receives sub-standard or no care will die. The idea that aging Americans would be allowed to languish without proper care when they are at their most vulnerable is unthinkable from a human standpoint. Pro-active planning to find a long-term care solution is essential to your future health and financial well-being.

We can help you put a plan in place that includes accessing and paying for appropriate long-term care. We can review potential programs to help offset some of the costs while creating a legal plan to protect your assets from the high costs of care. If you have questions or would like to discuss your personal situation, please don’t hesitate to contact us at (321) 729-0087.

Related Posts